CVV vs CVV2 is one of those things most people see every day but rarely understand. You’ve probably typed those three digits dozens of times when paying online, but never really stopped to think about what they actually do by carding legends .

In 2026, where online payments are everywhere and fraud is getting smarter, these small numbers play a bigger role than most people realize. They are one of the simplest but most important layers of protection between your money and cybercriminals.

At first glance, CVV and CVV2 sound like the same thing. And honestly, they are closely related. But there are subtle differences in how they are used, especially when it comes to online transactions and payment verification.

Understanding CVV vs CVV2 isn’t just technical knowledge it’s practical. It can help you avoid scams, understand how your card is protected, and make smarter decisions when entering your card details online.

What Is CVV?

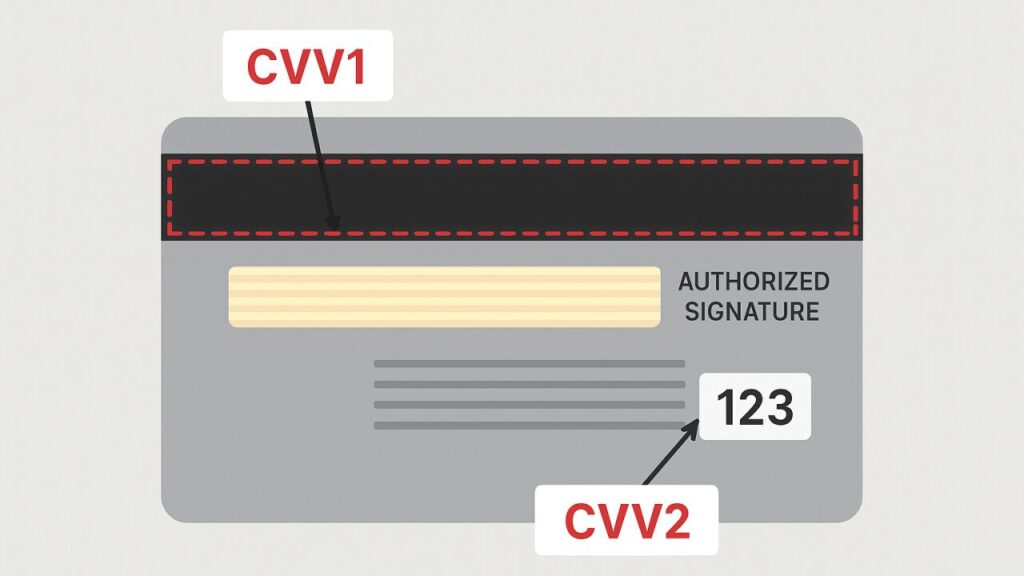

CVV stands for Card Verification Value. It’s a security code linked directly to your credit or debit card.

For most cards, it’s a 3-digit number printed on the back, usually near the signature strip. On some cards like American Express, it appears on the front and has four digits.

This code is not part of your card number, and it’s not stored in the same way either. It’s designed specifically to add an extra layer of security during transactions.

The main purpose of CVV is simple:

to confirm that the person making a transaction actually has the physical card.

So even if someone gets your card number, they still need the CVV to complete most online payments.

To understand how card details are abused, read our guide on online credit card fraud.

What Is CVV2?

CVV2 stands for Card Verification Value 2. It’s essentially an extension of the original CVV system, created specifically for card-not-present transactions meaning online or remote payments.

In real life, when you swipe or insert your card, the system verifies it through the chip or magnetic strip. But online, there’s no physical card.

That’s where CVV2 comes in.

It acts as a second-level check to confirm that:

- You have the card in your possession

- You are the legitimate cardholder

Even though CVV and CVV2 often refer to the same printed number, the difference is more about how and where they are used.

CVV vs CVV2: The Real Difference

This is where most people get confused.

Technically, CVV and CVV2 can refer to the same digits on your card. But the distinction comes from context and usage.

- CVV is the general term for the security code

- CVV2 is specifically used for online and remote transactions

Think of it like this:

CVV is the concept.

CVV2 is the application.

In modern payment systems, especially in 2026, CVV2 is what most platforms refer to when asking for your security code during checkout.

You can also learn how to stay safe in our article on protecting your credit card.

Simple Comparison

| Feature | CVV | CVV2 |

|---|---|---|

| Meaning | Card Verification Value | Card Verification Value 2 |

| Purpose | General security code | Online transaction security |

| Where used | Physical + digital context | Mainly online payments |

| Printed on card | Yes | Yes (same number) |

| Main function | Verify card authenticity | Verify card-not-present transactions |

Where to Find CVV and CVV2 on Your Card

Most cards follow a standard layout.

On Visa and Mastercard, the CVV/CVV2 is located on the back of the card, usually the last three digits near the signature strip.

On American Express cards, it’s on the front, above the card number, and typically four digits.

No matter the card type, this code is intentionally placed in a way that makes it harder for someone to access unless they physically have the card.

Why CVV and CVV2 Are Important

These codes are one of the simplest forms of fraud prevention, but they’re still very effective.

They protect you in situations where:

- Your card number is leaked

- Your card is copied digitally

- Someone tries to make an online purchase without your card

Without the CVV or CVV2, many payment systems will reject the transaction.

That’s why scammers always try to get both the card number and the security code. One without the other is often useless.

If you notice unusual activity, check these signs of credit card fraud.

Can Someone Steal Your CVV?

Yes — and that’s where things get serious.

Your CVV can be exposed through:

- Phishing websites

- Fake checkout pages

- Data breaches

- Malicious apps

Once someone has your card number, expiry date, and CVV, they can attempt online transactions.

That’s why you should never share your CVV casually, even if a website looks legitimate.

Is CVV the Same as a PIN?

No — and this is a very important distinction.

Your PIN (Personal Identification Number) is used for:

- ATM withdrawals

- In-person transactions

Your CVV/CVV2 is used for:

- Online payments

- Remote transactions

You should never confuse the two, and you should never share your PIN online.

Even digital wallets rely on similar protection systems, as explained in mobile wallet security practices.

Why CVV Is Not Stored by Merchants

Here’s something most people don’t know.

Legitimate websites are not allowed to store your CVV after a transaction.

This is part of global security standards (PCI DSS).

That’s why you have to re-enter your CVV every time you make a payment — even on trusted platforms.

It may feel inconvenient, but it’s actually protecting you.

How Fraud Is Evolving in 2026

Even though CVV and CVV2 are strong security layers, fraud is evolving.

Scammers are now using:

- Fake payment pages

- Social engineering

- Data leaks

In some cases, they don’t even need to hack systems — they trick users into giving away their details.

That’s why understanding how CVV works is more important than ever.

How to Protect Your CVV and Card Details

Keeping your card safe isn’t complicated, but it requires awareness.

Always make sure you are entering your details on trusted websites. Look for HTTPS and avoid suspicious links.

Never share your CVV over phone calls or messages, even if someone claims to be from your bank.

Avoid saving your card details on random websites.

Use banks or apps that offer transaction alerts so you can detect unusual activity quickly.

And most importantly, stay alert. Most fraud doesn’t happen because of weak systems — it happens because of human mistakes.

Some modern scams use social engineering to steal card details, as covered in AI voice scams.

Common Myths About CVV and CVV2

One common myth is that CVV and CVV2 are completely different numbers. In most cases, they are the same digits — just used in different contexts.

Another myth is that having your CVV means someone can access your bank account. That’s not entirely true, but it does allow them to attempt online transactions.

Some people also believe that hiding their CVV makes them completely safe. While it helps, it’s not enough if your full card details are exposed elsewhere.

The Future of Card Security

Payment systems are evolving fast.

In 2026, we’re already seeing:

- Biometric verification

- Tokenized payments

- AI fraud detection

But even with all these advancements, CVV and CVV2 are still widely used because they are simple and effective.

They may not be perfect, but they remain a key part of the security system.

Final Thoughts

CVV vs CVV2 might seem like a small detail, but it plays a big role in protecting your money.

These codes are not just random numbers — they are part of a system designed to make sure only you can use your card.

In a world where online payments are growing and scams are becoming more advanced, understanding how these security features work gives you an advantage.

Because at the end of the day, staying safe online isn’t just about technology.

It’s about awareness.

- 10 Signs of Credit Card Fraud

- AI Deepfake Voice Scams 2026

- Cybersecurity

- Dark Web Insights

- device fingerprinting

- DNS and OPSEC

- fraud detection

- Guides / Explainers

- online payment security

- online threats

- Prevention Strategies in 2026

- Privacy & Tracking

- Protect my credit card

- Safe Mobile Wallet Practices for Apple Pay

- security systems